Michael Ioane

Article IV

Summary Guide Article

Guide: Legal vs Tax Strategy

This guide provides a practical reference for navigating the distinctions and overlaps among legal strategy, tax strategy, and compliance in business and asset protection structuring. The frameworks here reflect Michael Ioane’s approach to designing structures that coherently serve all three dimensions, rather than treating them as independent or interchangeable concerns.

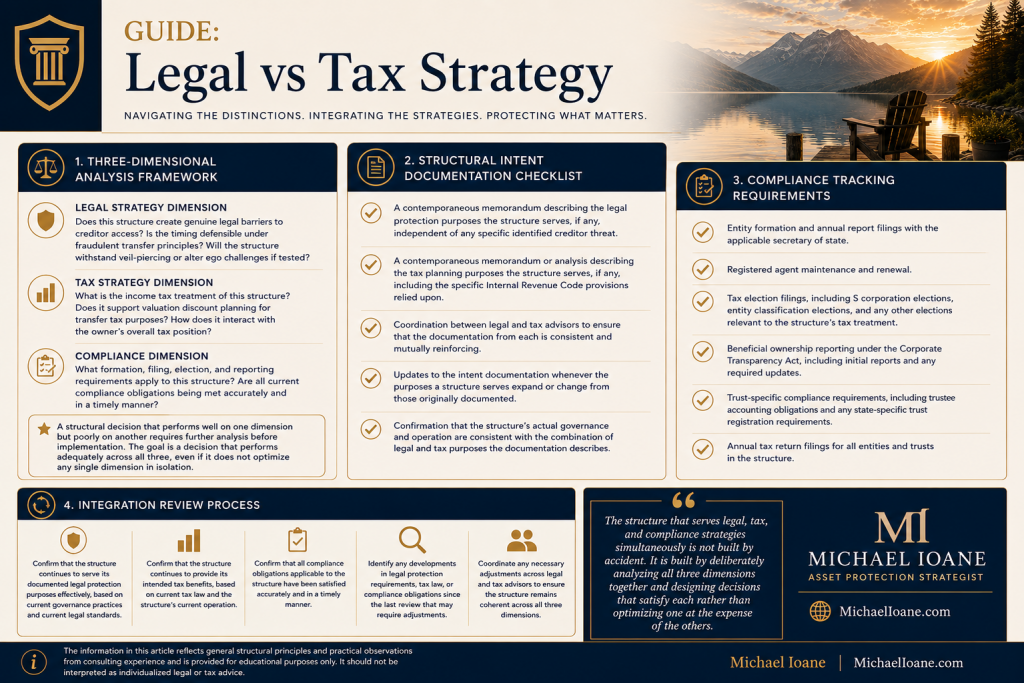

Three-Dimensional Analysis Framework

Evaluate every significant structural decision against all three of the following dimensions:

- Legal strategy dimension does this structure create genuine legal barriers to creditor access; is the timing defensible under fraudulent transfer principles; will the structure withstand veil-piercing or alter ego challenges if tested

- Tax strategy dimension: what is the income tax treatment of this structure; does it support valuation discount planning for transfer tax purposes; how does it interact with the owner’s overall tax position

- Compliance dimension: what formation, filing, election, and reporting requirements apply to this structure; are all current compliance obligations being met accurately and in a timely manner

A structural decision that performs well on one dimension but poorly on another requires further analysis before implementation; the goal is a decision that performs adequately across all three, even if it does not optimize any single dimension in isolation.

Structural Intent Documentation Checklist

Maintain the following documentation for every significant structural implementation:

- A contemporaneous memorandum describing the legal protection purposes the structure serves, if any, independent of any specific identified creditor threat

- A contemporaneous memorandum or analysis describing the tax planning purposes the structure serves, if any, including the specific Internal Revenue Code provisions relied upon

- Coordination between legal and tax advisors to ensure that the documentation from each is consistent and mutually reinforcing

- Updates to the intent documentation whenever the purposes a structure serves expand or change from those originally documented

- Confirmation that the structure’s actual governance and operation are consistent with the combination of legal and tax purposes the documentation describes

Compliance Tracking Requirements

Establish and maintain a compliance tracking system that addresses the following categories for every entity and trust in the structure:

- Entity formation and annual report filings with the applicable secretary of state

- Registered agent maintenance and renewal

- Tax election filings, including S corporation elections, entity classification elections, and any other elections relevant to the structure’s tax treatment

- Beneficial ownership reporting under the Corporate Transparency Act, including initial reports and any required updates

- Trust-specific compliance requirements, including trustee accounting obligations and any state-specific trust registration requirements

- Annual tax return filings for all entities and trusts in the structure

Integration Review Process

Conduct the following integration review at least annually for every significant structure:

- Confirm that the structure continues to serve its documented legal protection purposes effectively, based on current governance practices and current legal standards

- Confirm that the structure continues to provide its intended tax benefits, based on current tax law and the structure’s current operation

- Confirm that all compliance obligations applicable to the structure have been satisfied accurately and in a timely manner

- Identify any developments in legal protection requirements, tax law, or compliance obligations since the last review that may require adjustments to the structure

- Coordinate any necessary adjustments across legal and tax advisors to ensure the structure remains coherent across all three dimensions

The structure that serves legal, tax, and compliance strategies simultaneously is not built by accident. It is built by deliberately analyzing all three dimensions together and designing decisions that satisfy each rather than optimizing one at the expense of the others.

The information in this article reflects general structural principles and practical observations from consulting experience and is provided for educational purposes only. It should not be interpreted as individualized legal or tax advice.

Michael Ioane | MichaelIoane.com