Michael Ioane

Article II

DEEP TOPIC ARTICLE

Structuring Ownership of IP

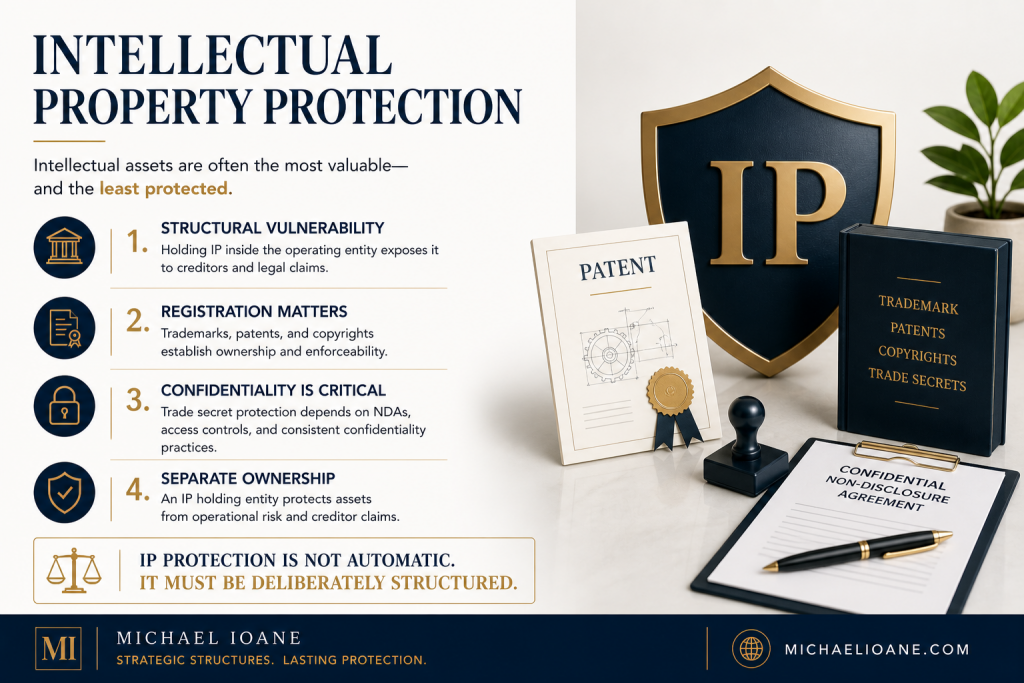

IP ownership structure is among the most consequential and least frequently addressed design decisions in business planning. Most businesses acquire intellectual property assets, whether through creation, development, or purchase, without deliberate attention to how those assets should be owned, who should own them, and what structure would best serve both the protection and the commercial development of the asset over time. The result is an IP ownership landscape that reflects historical accident rather than strategic design, and that creates vulnerabilities and inefficiencies that are expensive to correct after the fact.

Michael Ioane addresses IP ownership structure as a primary planning consideration in business engagements, because decisions made at an early stage compound in significance as the business grows and the IP becomes more valuable. A well-designed ownership structure implemented early lays the foundation for licensing, enforcement, and eventual transfer that serves the business owner’s interests throughout the business’s development.

Who Should Own the IP: The Core Design Question

The foundational question in IP ownership structure is who should hold legal title to each intellectual asset. The options include the individual owner, the operating entity, a dedicated IP-holding entity, a trust, or a combination of these. Each ownership arrangement has distinct implications for creditor protection, tax treatment, licensing flexibility, and transfer planning.

Individual ownership by the business owner provides the most direct control but exposes the IP to claims against the owner personally, including claims arising from activities outside the business. Operating entity ownership concentrates IP and operational risk in the same legal person, exposing the IP to business creditors. IP holding entity ownership separates the IP from operating risk, creates a dedicated licensing platform, and allows the IP’s value to be managed independently of the business’s operational performance. Trust ownership provides additional protection and estate planning benefits but requires more sophisticated governance. The correct answer depends on the specific IP assets, the business’s risk profile, and the owner’s long-term objectives.

The IP Holding Entity Structure in Detail

An IP holding entity is a separate legal entity formed solely or primarily for the purpose of holding and licensing intellectual property assets. In its most common form, it is an LLC with a professional management structure and governing documents that clearly define how IP assets are managed, how licensing agreements are entered into and administered, and how proceeds from licensing are distributed.

The IP holding entity licenses the IP to the operating entity under a written license agreement that specifies the scope of the license, the royalty or license fee, the term, and the conditions under which the license can be terminated. The license fee must be set at arm’s length, reflecting what an unrelated party would pay for the same rights. An artificially low license fee between related entities may be recharacterized by tax authorities, and an artificially high fee may be challenged as a mechanism for draining value from the operating entity. The licensing relationship between the IP holding entity and the operating entity must be genuine, documented, and consistently maintained at commercially reasonable terms.

Assignment and Work-for-Hire Considerations

A critical, and frequently overlooked, aspect of IP ownership structure is ensuring that the entity intended to own the IP actually does so as a matter of law. Intellectual property created by employees in the scope of their employment is generally owned by the employer. Intellectual property created by independent contractors is generally owned by the contractor, unless a written agreement assigns ownership to the hiring party. Intellectual property developed by a founder before the business entity is formed may be owned personally by the founder rather than by the entity.

Each of these ownership questions must be resolved explicitly through written assignments, work-for-hire agreements, and IP assignment clauses in employment and contractor agreements. An IP holding entity that purports to own IP that was never formally assigned to it does not actually own that IP, regardless of the entity’s governance structure or the owner’s intent. Michael Ioane treats IP ownership verification and formal assignment as prerequisite steps before implementing any IP protection structure.

Licensing Structure and Revenue Management

The licensing structure between the IP holding entity and its licensees determines both the protection the structure provides and the commercial efficiency with which the IP generates value. A well-designed license agreement defines the specific rights granted, the geographic scope, the field of use, the royalty calculation methodology, the reporting and payment obligations, and the audit rights that allow the licensor to verify that royalties are being calculated correctly.

For a business owner who licenses IP to both a related operating entity and, potentially, third-party licensees, the licensing structure must accommodate both relationships on commercially consistent terms. Related-party licenses at terms that no unrelated party would accept are a compliance risk from a tax perspective and a governance risk from a legal perspective. The IP holding entity must operate as a genuine licensing business, with the administrative infrastructure, the governance records, and the licensing economics that a genuine licensing business would have.

IP ownership structure is not an administrative detail. It is one of the most consequential design decisions in a business’s legal architecture because it determines who controls its most valuable assets and who can access them.

The information in this article reflects general structural principles and practical observations from consulting experience and is provided for educational purposes only. It should not be interpreted as individualized legal or tax advice.

Michael Ioane | MichaelIoane.com