Michael Ioane

Article IV

Summary Guide Article

Guide: Timing Strategies in Asset Protection

This guide provides a practical reference for applying timing strategies across all phases of asset protection planning. The frameworks here reflect Michael Ioane’s approach to planning timing, structuring timing, and the legal positioning decisions that determine whether protective arrangements will survive creditor challenge.

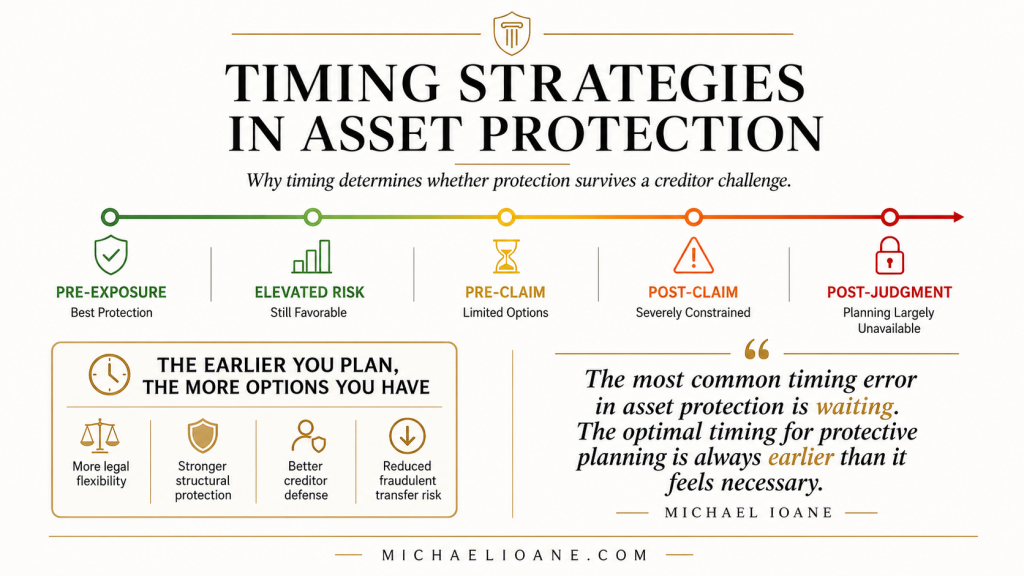

The Timing Spectrum: From Optimal to Unavailable

Asset protection timing exists on a spectrum defined by the client’s position relative to any creditor relationship. Understand the following positions on the timing spectrum:

- Pre-exposure planning (optimal): no existing creditors, no anticipated specific liability events, full freedom to implement all structural arrangements with maximum defensibility

- Elevated risk planning (favorable): no existing creditors, but exposure profile suggests increased future risk; all structural arrangements available with appropriate documentation of planning purpose

- Pre-claim planning (constrained): specific liability events have occurred, but no formal creditor claim has been filed; structural arrangements may still be available but require heightened documentation and careful analysis of applicable look-back periods

- Post-claim planning (severely constrained): creditor claim has been filed or demand received; most structural arrangements carry significant fraudulent transfer risk; only exemption maximization and existing structures remain fully available

- Post-judgment planning (effectively unavailable): judgment entered and enforcement underway; structural planning is largely unavailable, and existing structures must be defended rather than modified

Planning Timing Decision Framework

Apply the following decision framework when evaluating the timing of each structural component:

- Assess the current position on the timing spectrum for each asset category and each type of potential creditor

- Identify the planning windows that remain open and the windows that have already closed

- Prioritize the implementation of structures addressing the highest-value, highest-vulnerability assets while the planning window is open

- Document the business purpose and planning rationale for each structural implementation contemporaneously with execution

- Record the financial condition of the transferor at the time of each significant transfer to establish solvency and absence of fraudulent intent

- Confirm that each implementation predates any specific creditor claim by the longest feasible period

Structuring Timing Checklist

Confirm the following timing requirements for each structural implementation:

- Entity formations and initial asset contributions completed before any relevant liability events have occurred

- Trust implementations completed and look-back periods fully elapsed before any significant creditor risk has materialized

- Jurisdiction selection made before formation, accounting for both current and anticipated future statutory protections

- Intercompany agreements executed contemporaneously with the commencement of intercompany relationships

- Governance protocols established at the time of formation, with records commencing from the date of first operation

- Statutory exemption maximization initiated as early as possible, with contributions to exempt accounts maintained consistently from the date of implementation

Look-Back Period Reference

Account for the following look-back periods in timing all structural implementations:

- UVTA (Uniform Voidable Transactions Act): four years from the date of transfer for constructive fraud; four years from discovery or one year from when the transfer was reasonably discoverable for actual fraud, whichever is later

- Federal bankruptcy: two years for actual fraudulent transfers under 11 U.S.C. § 548; state law look-back period for constructive fraud under § 544

- Self-settled trust statutes (DAPT states): vary by state; Nevada and South Dakota impose two-year look-back periods from the date of transfer for existing creditors

- IRS: unlimited look-back for fraudulent transfers to which the IRS is a creditor; standard collection statute of limitations is ten years from assessment

Common Timing Errors to Avoid

Address the following timing errors before they become creditor vulnerabilities:

- Implementing protective structures after receiving a demand letter or learning of a potential claim without first consulting qualified counsel on fraudulent transfer exposure

- Modifying existing structures in response to financial difficulty, which can restart the look-back period analysis for the modified components

- Failing to account for future creditor relationships when timing current transfers, particularly for owners in high-liability industries

- Deferring implementation until the right time without recognizing that the optimal timing window may close before the deferral ends

- Assuming that a transfer made before a lawsuit was filed is automatically protected without analyzing whether the creditor relationship had formed earlier through the underlying events giving rise to the claim

The most common timing error in asset protection is waiting. The optimal timing for protective planning is always earlier than it feels necessary and later than it will ever be again.

The information in this article reflects general structural principles and practical observations from consulting experience and is provided for educational purposes only. It should not be interpreted as individualized legal or tax advice.

Michael Ioane | MichaelIoane.com